Hacker News Comments on

Economics of Money and Banking

Coursera

·

Columbia University

·

6

HN points

·

26

HN comments

Hacker News Stories and Comments

All the comments and stories posted to Hacker News that reference this url.https://www.coursera.org/learn/money-banking is an extroardinary introduction on what is actually money and how banking works (including the role of central banks)

Perry Mehrling's course Economics of Money and Banking

⬐ ipnonI found this to be the best introduction because it shows how every function of the money markets is a direct patch for a previous catastrophe. It balances the Wall Street view with the Ivy League view, and shows what happens when they butt heads. His book “The New Lombard Street” is more or less this course as a book, but covers more of the historical developments.⬐ DalekBaldwinI find it to be the best introduction because it draws on material from economists of different major schools of thought without requiring the student to subscribe to any school in particular. He can do that because he focuses on the structure of the modern financial system, which is neglected or abstracted away in most mainstream and even heterodox economics literature. It makes it easy to recommend this course to anybody, because they can't say "I'm sorry, this is from the toilet-water school of economics, and I only listen to the bilge-water school."

This course covers central banking in great detail: https://www.coursera.org/learn/money-banking.

Looks fantastic. Thanks.https://www.coursera.org/learn/money-banking

https://www.amazon.com/Economics-Banking-Financial-Markets-B...

Economics of Money and Banking [1] is what you’re looking for, especially if you’re interested in a historical narrative of the monetary system.

For rather deep dive: https://www.coursera.org/learn/money-banking/home/welcomeSomething shorter: https://gendal.me/2013/11/24/a-simple-explanation-of-how-mon...

Everything is inverted from the bank perspective. When they receive "cash" they actually receive an obligation to pay one of their client against some other debt, which might not be an enviable position.There is no such thing as digital cash actually. You have cash, the real and physical and all the rest is balance sheet expansion, i.e. debt.

If you are interested in banking I would encourage you to watch this course from the Columbia university: https://www.coursera.org/learn/money-banking which is the reference and is fascinating.

Yep, and it's not some new-fangled form of finance, it is the entire history of finance. There is a hierarchy of money, and it has always been so.I highly recommend this Coursera course to shed light on this: https://www.coursera.org/learn/money-banking

> 2 of the 3 dollars in your pocket have been created out of thin air in 2020.Dollars in your pocket (not 70%, but 100% of them) have been created out of paper, after a swap of figures on a balance sheet (that you call “thin air”). The number of paper dollar didn't increase by ~70% this year, what did is an economic aggregate called M1 which is a conventional (since the sixties) way of counting certain things. It ISN'T some fundamental value of what-money-is®. Most of the dollar every American own (their bank account, and their savings) have never been part of M1, so this money wasn't affected either.

The monetary system is a complex thing, and the landscape is changing at a fast pace since 2008, which makes it even harder to graps. Unfortunately, most cryptofans didn't even try to understand it, and they keep parroting the almost 100 years-old Autrian critique of central-banking without any kind of cognitive effort: “It's obviously broken, so I'm not going to try understanding it”.

For people without prejudices, interested in understanding the subject, I strongly recommend Perry G Mehrling's lecture on the Economics of Money and banking on coursera: https://www.coursera.org/learn/money-banking

⬐ gnusty_gnurc> and they keep parroting the almost 100 years-old Autrian critique of central-banking without any kind of cognitive effortJust naming something doesn’t invalidate it.

⬐ yaacov⬐ seibeljNaming something tells you what to look for in the academic literature (or even Wikipedia), where you will find in this case that the academic consensus has mostly moved on from the view named here⬐ gnusty_gnurc> the academic consensusThe academic consensus is a proxy for cultural elite; the condescending narcissists and effete.

Nothing reeks of moral superiority like brushing away opposition as "uneducated."

⬐ virgilpNow I'm not sure if you're still talking about BTC or we switched to vaccines...⬐ blaser-waffleSomeone is coming up with these theories, and it usually isn't Joe the Plumber.Most propaganda & marketing campaigns are coming out of well educated folk. Look into the Heritage Foundation, for example...

Economics is not a very difficult subject. Most people intuitively grasp supply and demand and other basics.What mainstream economics has tried to convince us is that hard work is meaningless and infinite money can be printed. Scarcity is a myth. I don't need complex graphs to explain away why printing shitloads of money causes inflation and warps incentives. It's hilarious that Keynesians keep pushing the same garbage and being surprised when people respond by purchasing scarce assets like Bitcoin. What did you expect would happen?

⬐ NikolaeVarius⬐ keymone> Economics is not a very difficult subjectI can't believe its possible to be so wrong.

The history of humans might as well be "getting economics less wrong than last time"

⬐ seibelj⬐ chalstEconomics is not complicated. It is people who try to confuse us by wrapping mismanagement in the veneer of econometrics and "science" that try and make confusing what is actually relatively simple.Both the US and Japan have ran enormous fiscal surpluses for decades with low inflation. How does your plain, simple intuition account for this gap between what you say must happen and what has happened?⬐ hykoScarcity is a mythI know of no serious economic school that espouses this.

⬐ NoOneNew⬐ ashtonkemThe idea conveyed here is that scarcity being the foundation of value is a myth. No economist believes that just because something happens to be rare makes it inherently valuable. I dont think any real economist really believes that. I think it was a pop culture, snake oil salesman thing that brought it into the zeitgeist. Yet to this day, the myth still prevails and bitcoin is mostly based on that concept. Just because something is "limited" doesn't mean it already has value.⬐ SAI_PeregrinusScarcity is necessary but not sufficient for something to have value. There are plenty of rare things that are worthless. Various forms of toxic waste, for example, aren't particularly common and have negative value.Keynes actually had a nice quip for things like Bitcoin:> The market can remain irrational longer than you can remain solvent.

⬐ whimsicalismThere used to be massive economic crises all the time while people still were using your "intuitive" grasp of economics.The truth is that inflation expectations were in the hole [0], and the Fed action restored inflation and price stability as per its mandate.

> M1 is the money supply that is composed of physical currency and coin, demand deposits, travelers' checks, other checkable deposits, and negotiable order of withdrawal (NOW) accounts.

I took a bunch back in the day, and I liked Economics of Money and Banking[1] (by Perry Mehrling) more than most other courses. It's partly a history of the American financial system, and partly a tour of some modern financial instruments and institutions. The focus is on how things work and why they're designed as they are, and not so much on how things are priced. Deposits, bonds, commodity futures, central banks, how it all fits together, what purpose it all serves -- how it's not just gambling or an abstract game used to extract money from the productive economy.One of the stated aims of the course is to get you in a position where you can read the Financial Times without going cross-eyed, and it works really well to give a clarifying framework for understanding market concepts outside the course's scope.

Another I really liked was "The Modern and the Postmodern" by Michael Roth. I don't know if that course would work well "at your own pace" though, the reading and peer essay feedback was a big part of it.

⬐ littlestymaarI came here to recommend the same course. It's really well done and covers not only conventional banking but also covers quantitative easing post financial crisis. And the guy is also pretty funny.⬐ avyfainI did "The Modern and the Postmodern" last year, and really enjoyed it without doing the essays/peer review. Curiously I'm now working through Mehrling's course, too.Another one I'd recommend if you enjoyed those two, although in a very different vein is Bloom's Moralities of Everyday Life, which is supposedly a psychology course, but really goes into comparative culture questions that IMO make it closer to an anthropology course. https://www.coursera.org/learn/moralities

Economics of Money and Banking by Perry Mehrling - https://www.coursera.org/learn/money-bankingGreat course to learn about monetary systems, central banks and its effects on financial markets.

I'm currently taking the "Economics of Money and Banking" course on coursera [0] and, as far as my understanding has developed, the Fed injecting cash is not an irreversible thing.When the liquidity crunch is over, the Fed will start gradually increasing the rate. That will make rolling over existing overnight loans taken from the Fed less attractive and a lot of money will flow back to the Fed.

I hope people more familiar with the subject will correct me if I'm wrong.

⬐ barry-cotterThe Fed and other central banks have almost total control over nominal inflation because they control the printing presses. They can create money by buying bonds and destroy it by selling them. They have bugger all control over real inflation but that’s a matter for the fiscal authorities to try and deal with by demand management.“Inflation is always and everywhere a monetary phenomenon.” Milton Friedman

Edited to fix elementary mistake as pointed out by forkerenok

⬐ radford-neal⬐ nscalfThat's mostly true (except as another comment says, the "sell" and "buy" are backwards).Certainly the central bank can create as much inflation as it wants, by simply printing and distributing more money (which usually takes the form of the central bank buying assets such as bonds with the new money). There's no limit to the ability of the central bank to make the currency valueless.

In the other direction, they can usually increase the value of money (ie, create deflation) by reducing the money supply, but it is possible that at some point the public might simply stop regarding the government's money as being worth anything. The only thing that might stop that is that people would still need government money to pay taxes.

⬐ forkerenok> They can create money by selling bonds...Did you actually mean it the other way around as in they can create money by buying govt bonds/treasury bills/etc and retire them by selling them back to the market.

⬐ barry-cotter⬐ tathougiesYes, will edit. Thanks.> The Fed and other central banks have almost total control over nominal inflation because they control the printing presses.Not quite true. Every bank can print money (well, the modern day equivalent of increasing a digital number somewhere), and does so when they make loans.

⬐ littlestymaarThat's funny to quote Milton Friedman in 2020 because the monetarist analysis have had zero predictive power since the 80s!⬐ barry-cotterYes, if you stop doing the thing that reliably leads to hyperinflation you don’t get any more hyperinflation.⬐ littlestymaarFirst of all, inflation and hyperinflation are two really different things. The first one being common in history while the second one is rare but catastrophic.Then, In Friedman's book inflation is related to the amount of money in circulation, yet since the 80s the amount of money and inflation have almost zero correlation in the US. Some of Friedman's concepts were useful to reach that point, but still: we now have been living for 40 years in a world where Friedman's model is unable to explain anything.

⬐ jfengelWe've never had hyperinflation in the US. We've had high inflation, but never hyperinflation. And we've had very low inflation since the 80s, including during the decade-plus period of practically-zero interest rates.Hyperinflation is a completely different issue from inflation, and it's kind of odd for it to become the monetarist bugaboo. When the US has a massive war debt payable immediately, or a complete economic collapse that the government decides to cope with by price controls, then you'll see hyperinflation. But then, hyperinflation will be the least of your problems.

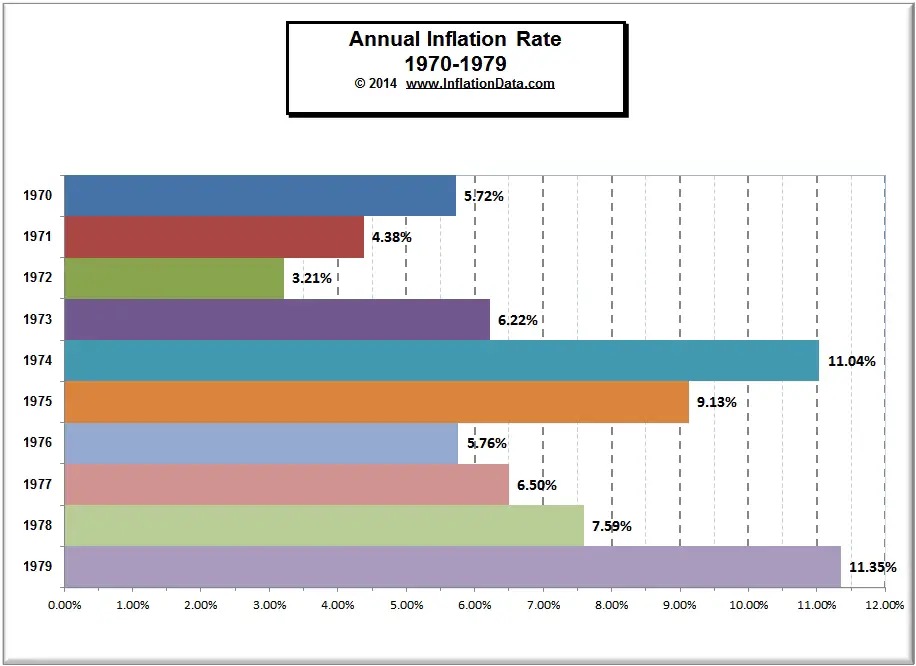

⬐ AnimalMuppetWell... the 1970s weren't a hyperinflation, but we were trending there. Inflation was not only high, it was increasing. Would we have wound up at hyperinflation if Volcker hadn't clamped down at the Fed? I don't know; that's alternate history. But it felt like we were headed there.⬐ None⬐ gphNone⬐ littlestymaarI'm sorry, but this is just wrong: inflation was high but fluctuated a lot and by no way you can say it was “increasing”. You're rewriting history in favor of your political bias.Inflation in the 70s (chart): https://inflationdata.com/articles/wp-content/uploads/2014/0...

⬐ AnimalMuppetI'm sorry, are you psychic? I didn't say anything about a political bias, nor anything to even hint at one. You're making up stuff that you think you know about me, with no basis.To the data: I agree that there are fluctuations there. But average inflation for the decade of the 1960s was 2.45%. For the 1950s, it was 1.82%. The inflation rate even for 1972 was above the average rate for the 1950s and 1960s. 1976, the bottom of the next trough, was higher than 1972. And then you look at 1974 and 1979, in the context of the 1950s and 1960s, and yes, it sure does look like inflation is increasing. Yes, there are decreases (business cycle), but each cycle is higher than the last one.

Not technically the US, but the Confederacy did experience hyperinflation during the war. They ran the printing presses at full-tilt without anything tangible to back them up. And obviously once the tide of the war shifted things got real bad.⬐ nostrademonsAlso not technically the U.S, but during the Revolutionary War the continental dollar underwent hyperinflation, leading to the phrase "not worth a continental". By the end of the war they were worth less than 1% of face value and had ceased to circulate as money.Currently the issue is that the fed has removed the overnight liquidity requirements. This opens up the threat of a bank run. All of this is due to years of aggressively propping up the economy for political means, in reality we should have had a market decline a few years ago, but the government massively mismanaged their responsibilities and pushed us into more than one bubble, while hamstringing their ability to respond.⬐ littlestymaarSince most payments are now dematerialized in developed countries, a bank run would cause little issue in practice though.⬐ lolcThe problem with a bank run is not the physicality of it, but the insolvency.⬐ csenseIf you're not transacting for physical cash, isn't your money going directly into an account at another bank?Unless people are withdrawing mass amounts of cash, I'm relatively certain you can't have bank runs against the banking system as a whole, you can only have runs against a particular bank.

⬐ coldteaWithout physicality though, it's not hard to restrict automatically the demand. Capital control measures...⬐ dmurdochMajor US banks will NOT be rendered insolvent. The fed won't allow it. They are literally too big to fail. They'll just be bailed out.⬐ chalstUS banks have deposit insurance of $250k per account for retail banks.⬐ protein_lenseYes, and in 1Q2017, the fund held $84.9E9. Meanwhile, in the US, gross private savings total $4.64 trillion, while personal savings total $1.06 trillion.(Sep 11, 2019)What happens when a major bank goes under and completely depletes the FDIC fund? (e.g. Bank of America)

Another key aspect of monetary metals is lack of counter party risk. When you deposit money with BoA, it is no longer yours; you become an unsecured creditor of the bank. BoA's derivatives counter parties are senior to you, so they will get paid first if say interest rate swaps go against BoA, and they need to post more collateral to that counter party.

Also, the problem with rates 'normalizing' is the magnitude of outstanding Treasury debt, and the fraction of GDP that the interest payments represent. 5% would be devastating, even though historically, that is a typical rate.

{kind=link}

This is the best online course I've ever taken:https://www.coursera.org/learn/money-banking

The professor explain the financial system very well using fairly recent and historic events.

This is an online course, not a book, but it changed my understanding of finance. I studied Economics (initially) at university, and never found anything close to as useful as this class:

⬐ samvherStarted this course based on your recommendation, and agree that it's very good. A lot of mysterious stuff (repo, LIBOR, fractional reserve banking) is making a lot more sense to me now.⬐ irlnCompletely agree, most texts concentrate on teaching outdated fractional reserve based monetary systems. Fractional reserves are no longer the major constraint on an expanding/contracting money supply. This course builds up an understanding of the push/pull factors of modern finance and banking.⬐ MerrillGreat course. It deals with the actual financial plumbing and how it has evolved from simple beginnings to the current complexity.⬐ mtrycz2Videos of one year's lectures are available on youtube, with links at here: https://www.ineteconomics.org/education/courses/the-economic...I'm halfway through, and I'm really impressed not only by the prof's preparation but methods. Very clear.

"Economics of Money and Banking" - https://www.coursera.org/learn/money-banking is a great course on the structure and operation of the money market, including repos. It's way more complicated that I ever imagined.The BIS report "September stress in dollar repo markets: passing or structural?" https://www.bis.org/publ/qtrpdf/r_qt1912v.htm

Economics of Money and Banking, taught by Perry Mehrling on Coursera:https://www.coursera.org/learn/money-banking

It's just fantastic. He explains what money really is from the perspective of treating everyone as a bank. Also, lots of good history here including the history of central banking, the gold standard, and war finance.

Anyone who wants to understand money should take this course. It would be nice if more cryptocurrency enthusiasts learned this kind of monetary economics.

⬐ FreebootsBut muh deflation!⬐ dangCould you please not post unsubstantive comments here?

I'm self taught mostly from books and MOOCs and arguing with friends of mine who are actual economists. Perhaps my lack of formal economics training is another reason not to listen to me.If you're interested in going deep on this stuff, I highly recommend this MOOC:

https://www.coursera.org/learn/money-banking

He doesn't talk about basic income, but this class really helped me understand the nature of money and economic policy.

If you're curious about more about the economics of a deficit-funded basic income, I'm working on a paper about that. Here's the abstract:

https://drive.google.com/file/d/0B9KDLUTAOkduOXdNQWl3REw4eWc...

Feel free to email me if you're interested in reading the full paper. It's over 50 pages long, but it's not very mathy and should (hopefully) be accessible to non-economists.

I recommend Perry G Mehrling [Columbia], (free) course on coursera [1] called Economics of Money and Banking. It provides a great context for how the current monetary system works. This context helps a bunch when comparing it to crypto.[1] https://www.coursera.org/learn/money-banking/home/welcome

⬐ doctorcrocThank you for sharing. Crypto is an interdisciplenary field, and we (folks on HN) view it through the lens of CS, at the exclusion of the other ways to approach the field.Any other courses / topics you recommend?

⬐ irln⬐ alimw[1] Federal Reserve Economic Data (charting) - Treasure trove of data.[2] Balance sheet of the fed

[3] Access to all the flows of the US Money System

[4] Monthly Treasury Statement (MTS) - The Bank money flows of all accounts of the US Government

[1] https://fred.stlouisfed.org/

[2] https://www.federalreserve.gov/releases/h41/

[3] https://www.federalreserve.gov/releases/z1/current/

[4] https://www.fiscal.treasury.gov/fsreports/rpt/mthTreasStmt/b...

The course is great, but nothing I learned there about the nature of money seems to apply to cryptocurrencies (about which admittedly I know very little). Could that be your point? That bitcoin only looks like money if you don't understand what money is

You might like this course: https://www.coursera.org/course/money

The Coursera course "Economics of Money and Banking" is fantastic, and focuses on real-world mechanics rather than theory. You should be able to view archived lectures if there isn't an active course: https://www.coursera.org/course/money

https://www.coursera.org/course/money https://www.coursera.org/course/money2 I took the first of these and intend to take the second, which I think came out as Coursera's top course at one point. There's a lot to learn here about what money is and how banks operate. That necessarily involves a historical perspective.

What I often do is sign up for any Cousera class that I could conceivably be interested in. I do nothing when the course is live, since I don't care about the certificate (paid or unpaid). Having signed up for the courses, though, I have access to the content in the future and can pick and choose what to watch. I then come back to the course and can consume it rapidly and with a focus on the materials I care about.For example, https://www.coursera.org/course/money . I had no idea what in this course and its sequel were important to me. But then a bank mentions how Standard Treasury should understand repo markets, and then I watched the lectures on that topic.

So the idea of consuming courses in modules is very appealing to me, and honestly how I consumed most classes in college: the material prescribed was basically incidental to what I ultimately learned about the topic. I'm the type of person who gets really focused on some applied problem and then teach myself the, for example, CS, stats, measure theory, machine learning, etc, to do what I want on the problem.

Tangent: My only compliant so far is that the (pure) math I can find in MOOCs goes exactly to the point I stopped: advanced calculus and theoretical matrix algebra. I don't expect it to have the types of statistics classes I'd like (I majored in the topic) but I'm annoyed that I can't really find an analysis course...

⬐ rgjmThere's a functional analysis course at https://www.coursera.org/course/functionalanalysis. I've only skimmed the notes but they look pretty good, if a bit terse.In general I think the lack of higher mathematics classes is because it would be very hard to evaluate proofs in a MOOC setting.

⬐ Russell91Yea, it's really tough to find an analysis course. I looked around online for a long time and never found one. Ended up picking it up as a regular college class and learned a lot. I don't understand why nobody has bother recording analysis lectures and posting them as they have with other subjects. It seems the only autodidactic way to learn analysis at this point is to download a book and dive in. If you're looking for pure math though, http://www.extension.harvard.edu/open-learning-initiative/ab... is a really great Abstract Algebra course taught by Gross at Harvard though.⬐ swimfarWhile not a course in the udacity/coursera sense, I found these real analysis lectures by Professor Francis Su extremely good. He breaks down every step of the derivations. And while sometimes the questions he asks, or the things he states may seem trivial I think it helps to focus on these simple but very important details.

Interesting ! An excellent introduction is also available as a coursera class (by Perry Mehrling from Columbia U) at https://www.coursera.org/course/money and https://www.coursera.org/course/money2 !

⬐ polskibus+1 on the coursera classes, Mr. Mehrling is an amazing teacher and really knows the subject well. I finished part 1 of his course and am close to finishing part 2.