Hacker News Comments on

A Farewell to Alms: A Brief Economic History of the World

·

6

HN comments

- This course is unranked · view top recommended courses

Hacker News Stories and Comments

All the comments and stories posted to Hacker News that reference this book.The mention of Malthus always inspires me to recommend the best book I've read in the past few years:http://www.amazon.com/Farewell-Alms-Brief-Economic-History/d...

tl;dr: Malthus was right.

⬐ lotharbotMalthus thinks that population grows like the dark gray line in [0]. Verhulst, and pretty much everyone else who has studied population dynamics [1], thinks population grows like the light gray line (though perhaps with more complexity.) Notice the actual population data following the light gray line.[0] http://www.growth-dynamics.com/articles/Kurzweil_files/image...

[1] http://en.wikipedia.org/wiki/Logistic_function#In_ecology:_m...

⬐ Fuzzwah⬐ jakeonthemoveThis thread triggered a memory of a couple of amazing TED talks Hans Rosling presented:http://www.ted.com/talks/hans_rosling_shows_the_best_stats_y... http://www.ted.com/talks/hans_rosling_on_global_population_g...

Oh joy, he has a new TED talk posted in March that I haven't seen yet. Thanks!

No... no he wasn't...⬐ TDL⬐ nowarninglabelWould you care to elaborate. Which of hypothesis was Malthus right about and which was he wrong about?"No... no he wasn't..." adds no value to the discussion.

⬐ rprosperoAt the simplest level, Malthus predicted that the population would outpace food production by the mid 19th century. So, on that level, he’s objectively wrong.The main problems are the assumption that food production grows linearly and that population grows geometrically. For food production, scientific advances have kept food production growing far faster than linear. With future advances in technology, I could believe a 10x increase in food production in my lifetime. No one is predicting a population of 70 billion any time soon.

Also, the population isn’t growing geometrically. For the trivial answer, the growth has been more exponential. However, there have again been scientific advancements that Malthus simply couldn’t have forseen. Effective birth control keeps the population count lower. The switch from agrarian to urban culture has eliminated most of the advantages of producing large families and heavily rewarded producing smaller ones. In terms of hard facts, the world population growth rate has been declining since 1963. The UN’s medium projection of population growth predicts a population downturn by 2050.

At the basest level, he was right that the population can’t grow indefinitely. However, most claims that are more specific than that haven’t panned out.

⬐ gbogSo he was wrong because he had a too narrow view of the problem. I live in China, overpopulation means something here but even then any plane trip over any part of the world will show you, if washe weather allows, that humanity is not the cancer some describe.there is still plenty of room.Malthus was right about what? He was wrong about nearly every single main hypothesis he made! What are you saying he got right?http://www.economist.com/node/11374623 http://wmbriggs.com/blog/?p=1837

Have you actually read Malthus' works?

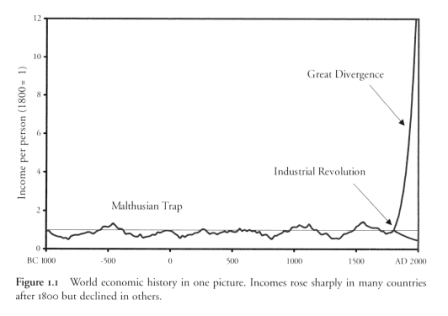

⬐ pauljonasUp until 1800, Malthus was spot-on -- any advance in technology that was greeted by population increase would snap back to an equilibrium, with war|disease|hunger inflicting the correction. Gregory Clarke goes into great detail, with statistics on caloric consumption, lifestyle, etc.. that show that the average person at the pre-dawn of the industrial revolution did not experience conditions much more favorable than those of Roman times.⬐ ojbyrneThe book I referenced basically says that western civilization is an aberration caused by a unique set of characteristics, and that the vast majority of people in the world still live in subsistence conditions. Also that the west could easily slip back into those conditions.⬐ mseebachBut what does that have to do with Malthus?⬐ ojbyrneThe book says that many 3rd world countries are in a "Malthusian trap" - any increase in income levels results in a population increase that overwhelms the higher income. Bangladesh is a good example.

{kind=link}

{kind=link}

"Atheism is making one of it's cyclical comebacks to popularity"?That's bad?

Also

"Over the past couple of millennia, the amount of work required simply to live has decreased dramatically, at least in the western world. It used to be almost your entire life was taken up simply in an effort to survive; now most of us work 40 hours per week and it takes care of all of our needs."

That's not really true. I suggest reading "A Farewell to Alms" (http://www.amazon.com/Farewell-Alms-Brief-Economic-History/d...)

A more accurate description would be something like "After several thousands of years where civilization has made life more difficult for the vast majority of people, over the last 200 years, in a few countries that have experienced the industrial revolution, the effort required to survive has returned to roughly the same level as required by paleolithic hunter-gatherers. Though with significantly longer life spans almost entirely due to a large reduction in infant and child mortality."

One of the more interesting books I've read recently - A Farewell to Alms - http://www.amazon.com/Farewell-Alms-Brief-Economic-History/d...has the basic argument that as a direct result of modern technology, there are people living on the planet now (in sub-saharan Africa), with the lowest standards of living ever present on this planet, significantly worse than that experienced by Paleolithic hunters and gatherers.

Uncivilized lifestyles turned out not to be that brutal, and in fact modern medicine is the primary mechanism by which the poorest countries have significantly lower standards of living than undiscovered tribes.

http://www.nytimes.com/2007/08/07/science/07indu.html

I'll reply to myself because I've just explained this sentence to myself:Because the government needs to run a deficit, it's the only way to inject financial resources into the economy.

The central fact of economics is: The economy grows. The number of people on earth is still growing. The productivity of individual workers is still growing. We are capable of making more stuff in every year than we did in the previous year.

Now, suppose the supply of money were finite. But the amount of stuff being made keeps getting larger. So, every year, the price of everything goes down, because there's an ever-larger supply of pizza and beer but a constant amount of money.

But this creates a serious problem for the economy. Because now we've got deflation. And that produces a really big incentive to save. Too big an incentive. Everything will be cheaper tomorrow, so every individual benefits by burying money in the backyard and spending as little as possible.

But as people bury more and more money, the economy shrinks, because there is less and less money to spend, and everyone is trying to hang on as long as possible without spending anything. You end up with lots of people sitting, unemployed, with tools idle, and resources idle, and money buried in the backyard, staring at each other and waiting for someone to make the first move. Because, thanks to deflation, the first person who spends anything is a relative loser. And now your economy has deadlocked.

And that's why the government always runs a deficit, and why the inflation target is always higher than zero. The government prints money to make sure that the supply of money stays good. This produces some amount of inflation, of course, but the growth benefits of liquidity outweigh the inconvenience of having to do something more interesting with your money than bury it.

(Why don't more people understand this? Partly it's because the growth of the economy is a historically new phenomenon, dating back only about 150 years. Before that, as far as we can tell, human economic production per capita barely grew throughout millennia of history:

http://www.amazon.com/Farewell-Alms-Economic-History-Princet...

The other cause for misunderstanding is that if you, say, define "gold" or "silver" as equivalent to money, and your society's economic productivity grows, but society's ability to dig up gold or silver grows exactly as fast as overall productivity at all times, the currency magically manages itself. Because of this, for a hundred years and more of the Industrial Revolution the world managed to struggle along with a gold-based money system. But, of course, the gold standard was abandoned when people finally figured out that this process is very haphazard -- indeed, it cannot be controlled. You can't discover gold overnight, but sometimes you need more money in the economy overnight. Like now, for example.)

⬐ megablastIf a country prints more money, then it makes the money it has worth less. So those with large foreign currency reserves in say, US dollars, will be worth less.Of course, when the US dollar is worth less compared to other currencies, then there is more of an incentive to export and produce locally, rather than import.

I am not convinced of your idea. The economy doesn't always need to grow, and can not always grow. This is how we get bubbles, when things start growing too fast, and it all collapses on itself.

⬐ lionheartedDude, m_f, you're normally one of my favorite posters on here and you say stuff that makes a lot of sense, but you've got some errors going on on this one:> But this creates a serious problem for the economy. Because now we've got deflation. And that produces a really big incentive to save. Too big an incentive. Everything will be cheaper tomorrow, so every individual benefits by burying money in the backyard and spending as little as possible.

That's basically just summed up modern macroeconomic thought right there. The problem is, it's wrong for a lot of reasons.

First off, deflation is a good thing - deflation means tomorrow you can get more for the same price. The industry in the most rapid deflation over the last 10 years has been the computer industry - you can much, much more computer for the same money now than you could at any point in the past. This is, by itself, a good thing.

Now, not everything is prone to deflation anyways, and you've got to realize that deflation lowers costs on both the producing and consuming side. So farmers are getting lower prices for their food gradually, but their tools and tractors are getting cheaper too.

But will the economy grind to a halt without new money coming into it? Well, the historical pre-central-banking answer is no of course, but why is that?

It's because people won't put their money under the mattress - they'll try to get their money (and thus, resources) producing more wealth for them.

Under a normal, sane, classical banking system, this is by giving it to a loan banker. What's a loan banker? He's someone you give your money to, who lends it out, but you can only get your money at certain times, not whenever you want. So you give him your $10,000, he says he'll give you back $10,000 + X in one year.

X is the interest you get paid. The loan banker charges the borrower interest for the money. Say, 10%. The borrower has to pay back $11,000 after a year. Then the banker gives, for easy math, let's say 5% to you. So you get back $10,500.

But wait - why doesn't the economy grind to a halt? Because the borrower spends the money, and increases productivity with it, thus paying back the loan. If he fails to, the banker collects the collateral and sells it to recover as much as he can. You risk your money by giving it to the banker, but if his operation is sound, it's not that much of a risk.

Anyway, loan bankers are extinct in the USA, we only have savings-and-loan banks, where you can get your money at any time. A bank where you could get your money at any time used to be called a deposit bank, but they didn't loan your money out for you, they kept it and transferred it to other people for you when you wrote a check. You actually paid to keep your money safe in a deposit bank, whereas loan banks paid you.

Mixing the two - your money is gone and loaned out, but you can collect it any time regardless - this is where the need for central banks originated. There was a landmark legal case in England about whether this mixed form of banking was fraud or not in the late 1600's, and the judge said it wasn't, and that's where today's banking system came from, but I think the judge made a mistake.

Long story really really short, you don't need to inject new money, people will loan it out very carefully into productive endeavors, and that's why all the non-central-banking economies throughout history didn't grind to a halt. True, they get slower growth in most years, but you also don't get the crippling nasty bank crashes that central banking creates.

⬐ gizmomagicoThere's no reason to assume that the random guy you quoted is right or even knows what he's talking about.Likewise, there's no reason to assume you know what you're talking about, this time, so why did you quote that post as if it's the ultimate truth on deficits, and why are you speaking as if with a voice of authority on the matter?

A lot of the people talking about the economy in the media say things that are aligned with their personal interests, and there's an endless supply of commentary that sounds plausible when you don't understand/know enough yourself, happens to be something you want to believe in, and is still nonsense, bullshit/lies, or just detached from reality.

⬐ poThese are great points you're making. And I think the way you are making them is very intuitive. It is impossible to default on a currency you control. You just print some more space-credits. I think you sum up why you should always be printing space-credits nicely.Reminds me a bit of what Paul Krugman has been saying over on his NYTimes blog: http://krugman.blogs.nytimes.com/

> Why don't more people understand this? Partly it's because the growth of the economy is a historically new phenomenon, dating back only about 150 years.

I personally think the reason people don't understand this is because they think that a government should be run the way a family should: save and don't live off credit.

Agreed that it's impossible to come up with a single concrete, satisfying answer to these questions. However we're not building a criminal case - it's more of a civil case, where the side with the preponderance of evidence wins. In that vein, two books that I found enjoyable were "Albion's Seed" (http://en.wikipedia.org/wiki/Albion%27s_Seed) which details how cultural differences in four areas of England manifested themselves in colonial America, with cultural consequences to this day; and "A Farewell to Alms" (http://www.amazon.com/Farewell-Alms-Economic-History-Princet...) which attempts to explain why England was the first country to escape the "Malthusian Trap", enabling the industrial revolution.

Ah, well, I studied at an IIT too, (Madras [Ganga] 98-02 shoutout! :) ) and I do agree that the pressure to jump examination hurdles is rather intense, but this again is a case of striving for very conventional goals, and for a limited period of time.How many have kept up the effort, after getting through (or not)?

As I said before, a conventional trajectory passing through a marriage in the mid-twenties, is also one that makes the uptake of risk (and consequently effort) much harder in life. I keep bringing up risk because effort without the possibility of significant success is rather pointless. And without risky opportunities that afford that kind of success, people reach for the cruise control after just-enough.

Malthusian scarcity should reward and select for effort, ( and also voluntary birth control and later marriage) as it did in the period right before Industrial England (([1] ; descriptive review: [2])), but, in India, it strangely doesn't! Predestiny, passivity, and fatalism, all predate socialist India. Our mythology reflects this.

I do agree that we are turning a new chapter and we are host to a whole new set of cultural ideas, but the numbers aren't, unfortunately, high enough. Yes, while about 300 million people, are (or were in 2001) technically urban, 50 million are slum dwellers; I'd wager that only a tiny slice is literate enough to accept cultural transmissions.

Still, I hope that this tiny slice of a humongous pie proves to be big enough....

[1] http://www.amazon.com/Farewell-Alms-Economic-History-Princet...

[2] http://www.nytimes.com/2007/08/07/science/07indu.html?pagewa...

⬐ randomwalkeri think i've seen you around :)⬐ ChaitanyaSaigood to see a co-alum here!, even if such an occurrence should be entire predictable :) ...